Merchant payments are the hottest battleground for digital financial services providers (DFS) in emerging markets. Over the last five years, mobile network operators (MNOs), fintech, FMCG brands, and other players have sought to crack merchant payments, and it’s easy to understand why.

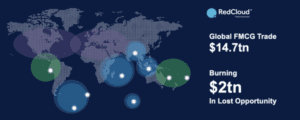

While much progress has been made with person-to-person (P2P) payments as an initial use case in many markets, retail payments are a much bigger prize, as small merchants accept $19 trillion in cash payments yearly. Digitizing these cash payments would unlock a massive and immediate opportunity for DFS and MNOS, nearly 500 times more than the total volume of payments made across the entire mobile money industry.

However, digitizing merchant payments and driving the adoption of the different types of digital payments in the retail market have proven a tough nut to crack for DFS and FMCG brands alike. This article provides a blueprint for digitizing merchant payments by adopting a strategy from the global card payments industry, which can help the digital payments industry unlock up to an additional $19 trillion in revenue.

Why digital payments?

The arguments for digital payments are well known by now; it’s faster, more secure, and cheaper than cash on a large scale. Currently, cash handling costs can reach up to 9% of the annual revenue of distributors, wholesalers, and consumer brands, while retailers lose up to 4.7% to 15.5% per transaction due to leakages and other cash management costs.

In addition, many merchants cannot pay for the products they need when the FMCG sales van comes around due to a lack of cash, leading to avoidable stock-outs on shelves and lost sales opportunities.

However, the most important component of digital payments is the massive amount of detailed transaction data generated. These data can be analyzed to identify trends and patterns in buying behaviors, and the insights generated can be used to create new products and services. These would help introduce value-added services, like credit facilities and insurance, that will benefit small merchants in some of the most vulnerable and disadvantaged communities across emerging markets.

Despite the seemingly obvious advantages of digital payments, merchant adoption rates remain abysmally low, and DFS cannot crack the code on merchant payments. The reason is a strongly held skepticism of digital payment solutions in the retail industry.

Why cash is currently better than digital payments

The simple reason merchants and small retailers prefer cash is a better customer experience. For most merchants, cash is free to use, universally accepted, reliable, and requires no prerequisites. In contrast, most digital payment solutions are cumbersome, have a steep learning curve, and require additional technology.

â€